There isn’t any denying Nvidia has been the centerpiece of the substitute intelligence (AI) revolution so far. Its expertise is used within the overwhelming majority of the world’s AI platforms just because it presents essentially the most computing energy. And Nvidia shares have carried out accordingly for the reason that motion bought stepping into earnest early final yr.

As is the case with every other business, nonetheless, time is driving modifications on the AI entrance. Nvidia is not the market’s prime alternative. This title is shifting towards Taiwan Semiconductor Manufacturing Firm (NYSE: TSM), which is arguably higher positioned to capitalize on the following chapter of AI’s progress story.

Taiwan Semiconductor is behind the scenes… all of them

Nvidia is not doomed. However it might be naïve to not acknowledge that the majority of AI’s simple cash has already been made. Competitors is heating up. Intel and Superior Micro Units are stepping up their video games. Worth wars are underway.

There’s an usually ignored however necessary element concerning the AI {hardware} enterprise you should perceive, nonetheless. That’s, chipmakers just like the aforementioned Nvidia and AMD often do not manufacture their very own chips. They sometimes outsource such work to third-party “contract” producers which can be able to fabricating this silicon to its designers’ specs.

Taiwan Semiconductor is certainly one of these contract producers. Certainly, it is the largest identify within the enterprise. It is estimated to fabricate on the order of two-thirds of the world’s semiconductors and related circuitry, and a fair better share when simply wanting on the planet’s high-performance chip market.

This may assist drive the purpose dwelling: Superior Micro Units in addition to Nvidia are each confirmed prospects of Taiwan Semiconductor. Intel continues to put money into the development of its personal foundries, though it is cast a developmental partnership with Taiwan Semiconductor to take action.

Join the dots. Taiwan Semiconductor may very well be the technological coronary heart and soul of the worldwide AI revolution.

And it isn’t restricted to knowledge facilities. As time marches on, AI computing work is making its method towards finish customers, and finish customers’ cell phones particularly. Apple‘s latest processor — the A17 discovered within the iPhone 15 Professional and Professional Max — is able to dealing with generative AI duties on the machine itself slightly than within the cloud, the place most generative AI work is presently performed.

It is not simply Apple wading into on-device synthetic intelligence waters, both. Qualcomm‘s latest high-performance Snapdragon 8 (Gen 3) cell processors can handle the same kind of load on cell units.

Apple in addition to Qualcomm each additionally make the most of Taiwan Semiconductor’s chip-manufacturing providers.

Nonetheless loads of alternative forward

Taiwan Semiconductor Manufacturing would not make each chip utilized by the aforementioned outfits, for the file, nor does it manufacture each AI chip the world’s at present utilizing or will use sooner or later. It is doubtless dropping market share as different gamers ramp up their capability to crank this silicon out, in truth. Intel particularly is displaying the potential to turn into a severe competitor to Taiwan Semiconductor.

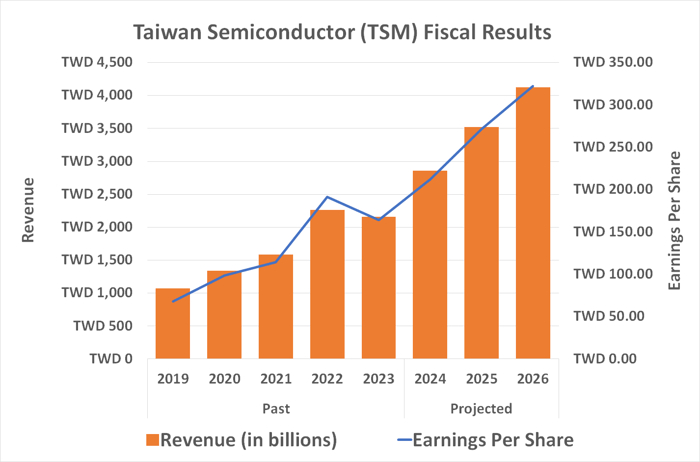

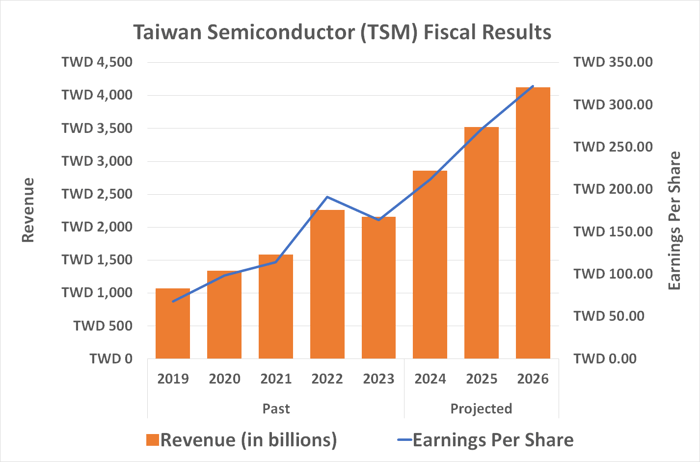

There’s nonetheless extra upside right here than not, nonetheless, regardless of the prospect of shrinking market share. Market analysis outfit Skyquest suggests the artificial intelligence {hardware} market is ready to develop at an annualized tempo of 15.5% by way of 2031, whereas the cell AI market is prone to develop at a compound yearly fee of almost 27% for a similar time-frame. On this vein, the analyst group believes Taiwan Semiconductor’s prime line is ready to just about double between final yr and 2026, because the AI chipmaking business gels.

Knowledge supply: StockAnalysis.com. Chart by writer. Figures are in new Taiwan {dollars}.

So why is that this inventory down greater than 20% simply since its July peak (with many different synthetic intelligence names down similarly)? That is bought extra to do with the market atmosphere than anything. Traders lastly started realizing final month that a couple of too many shares had reached too-frothy valuations. The disappointing jobs report for July launched on Friday of final week did not assist both, main the gang to presume lingering financial weak point is on the horizon.

And possibly it’s.

Do not lose perspective, although. Even in a tricky financial atmosphere most chip manufacturers are nonetheless going to wish new silicon. And most of them are nonetheless in no place to make a lot (if any) of it themselves. They’re going to nonetheless want Taiwan Semiconductor to make it for them. Certainly, financial weak point may even stifle capital expenditures on new foundries, making a confirmed, cost-effective foundry like Taiwan Semiconductor Manufacturing all of the extra necessary to the AI enterprise’s largest gamers.

Must you make investments $1,000 in Taiwan Semiconductor Manufacturing proper now?

Before you purchase inventory in Taiwan Semiconductor Manufacturing, contemplate this:

The Motley Idiot Stock Advisor analyst crew simply recognized what they consider are the 10 best stocks for traders to purchase now… and Taiwan Semiconductor Manufacturing wasn’t certainly one of them. The ten shares that made the lower might produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… for those who invested $1,000 on the time of our suggestion, you’d have $641,864!*

Stock Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Stock Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

James Brumley has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Units, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel and brief August 2024 $35 calls on Intel. The Motley Idiot has a disclosure policy.